This article on How to Trade Options on Micro E-mini Futures is the opinion of Optimus Futures.

- CME Group have announced the launch of Options on Micro E-mini S&P 500 and Micro E-mini Nasdaq-100 Futures

- There are hundreds of options trading strategies that you can use to take advantage of different scenarios.

- Micro E-mini Options strategies can range in complexity.

- It is important to know exactly how to calculate your potential risk and reward before engaging in any Option trades.

- Armed with solid options strategies, you can now explore more ways than just one to take advantage of these markets.

Images courtesy of Optimus Flow

16 Micro E-Mini Options on Futures Strategies:

Covered Call

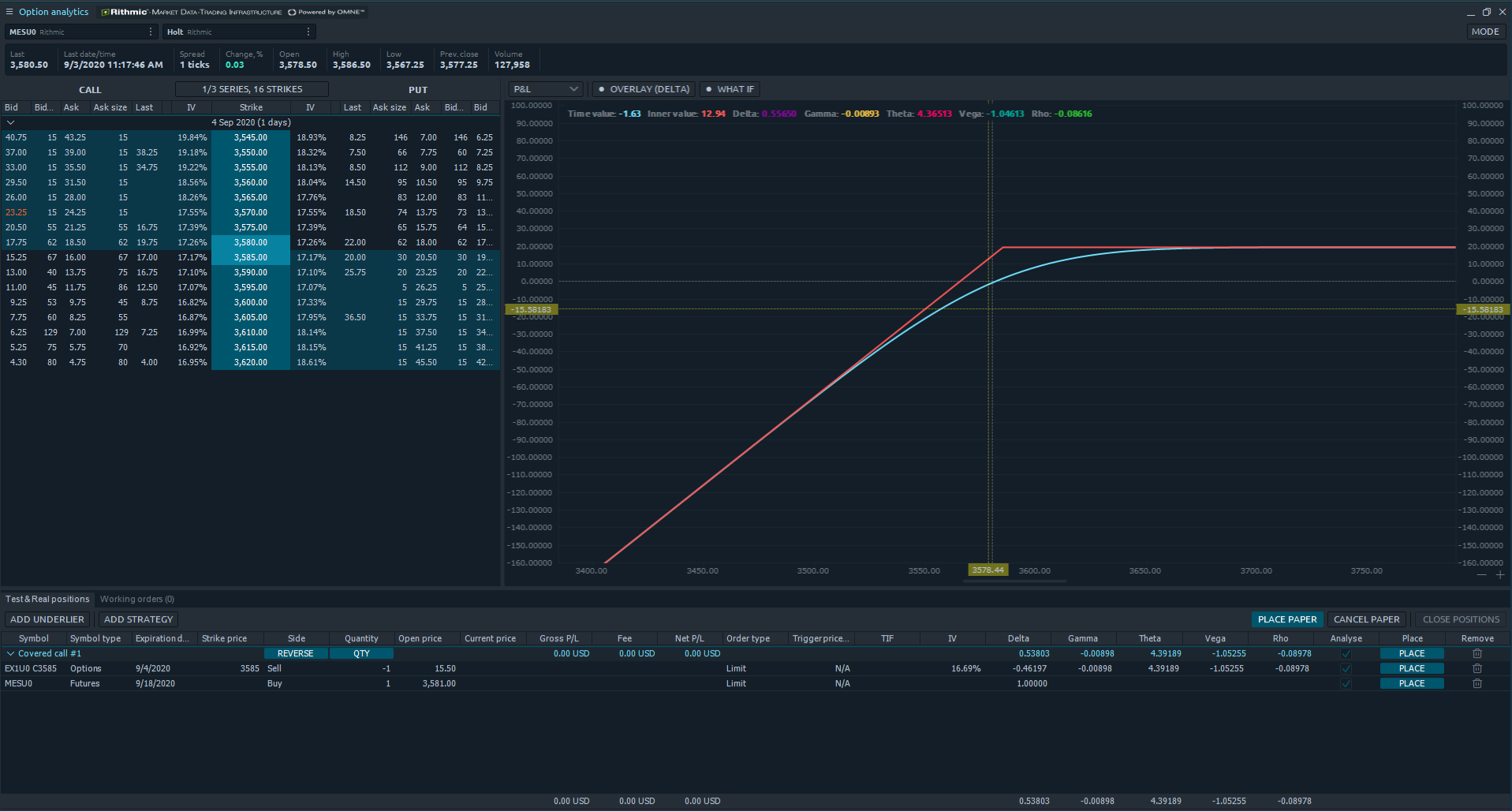

How to Construct It:

- Buy (or own) one futures contract

- Sell one OTM call at a strike price higher than your futures’ buy price

Objective: To collect income from the options premium, provide limited downside protection using premium income, all while capping potential gains should the futures exceed the option’s strike price.

Directional Bias: Bullish.

When to Use It: When you’re bullish on your futures position but wary of limited downside or sideways trading.

Profit Scenario: If your futures contract rises, you may receive profit on the decayed options premium; if the futures price exceeds the options strike price, your profit is capped.

Loss Scenario: If the futures trades lower, your profit from the options premium may offset some of your futures losses.

Key Concepts:

- Covered calls give you wiggle room in a loss scenario depending on the price of the premium at which you “sold short.”

- In a profitable scenario, your upside is limited due to your short options position.

- Time decay helps your position either way.

Covered Put

How to Construct It:

- Sell short one futures contract

- Sell one options contract OTM at a price lower than your futures sell price

Objective: To collect decaying premium while your futures contract is declining while adding limited protection should your futures rise in value.

Directional Bias: Bearish to neutral.

When to Use It: When you’re bearish on your futures position but wary of an upward reversal or unfavorable sideways trading.

Profit Scenario: If your futures contract declines, you may receive profit on the futures position plus the decayed options premium value; if the futures price falls further than the options strike price, your profit is capped. Calculation: (Shorted futures price – strike price) + put premium

Loss Scenario: If the futures trade higher, your profit from the options premium may offset some of your futures losses, but overall, your losses are unlimited.

Key Concepts:

- Covered puts give you wiggle room in a loss scenario depending on the price of the premium at which you “sold short.” But your risk is unlimited should the underlying continue higher.

- In a profitable scenario, your upside is limited due to your short options position.

- Time decay helps your position either way.

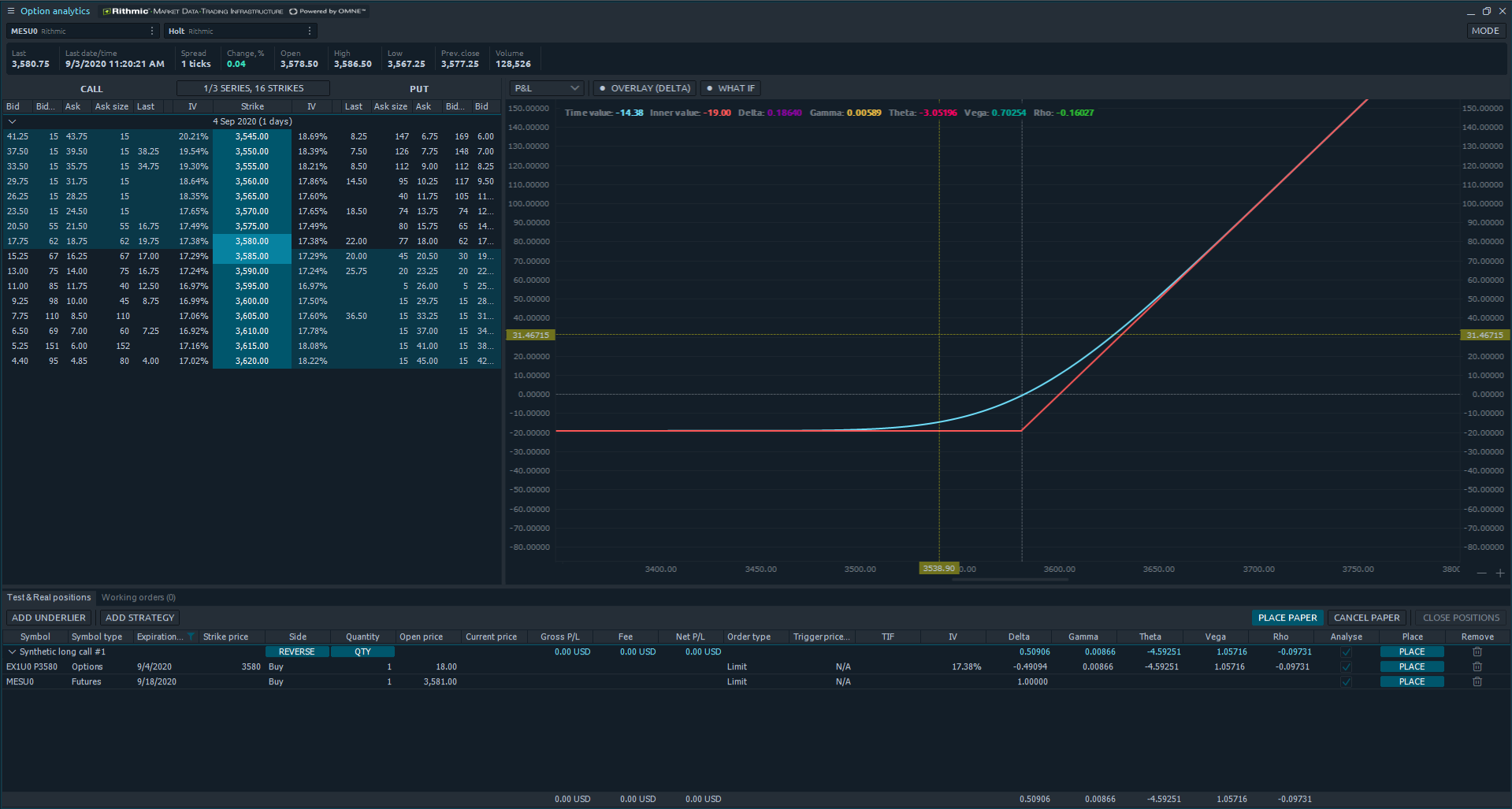

Synthetic Call

How to Construct It:

- Buy one futures contract

- Buy one ATM or OTM put.

Objective: To cap your downside should the futures fall.

Directional Bias: Bullish

When to Use It: When you’re bullish but want to be some “insurance” in case you’re wrong.

Profit Scenario: When your futures contract exceeds the premium you paid for your put, your upward profit scenario is uncapped.

Loss Scenario: If your futures contract falls, your loss will accumulate until it hits your put strike price. Calculation: Futures price + put premium – put strike price

Key Concepts:

- You profit the most if your futures contract has an explosive move upward.

- Your downside is limited by your long put.

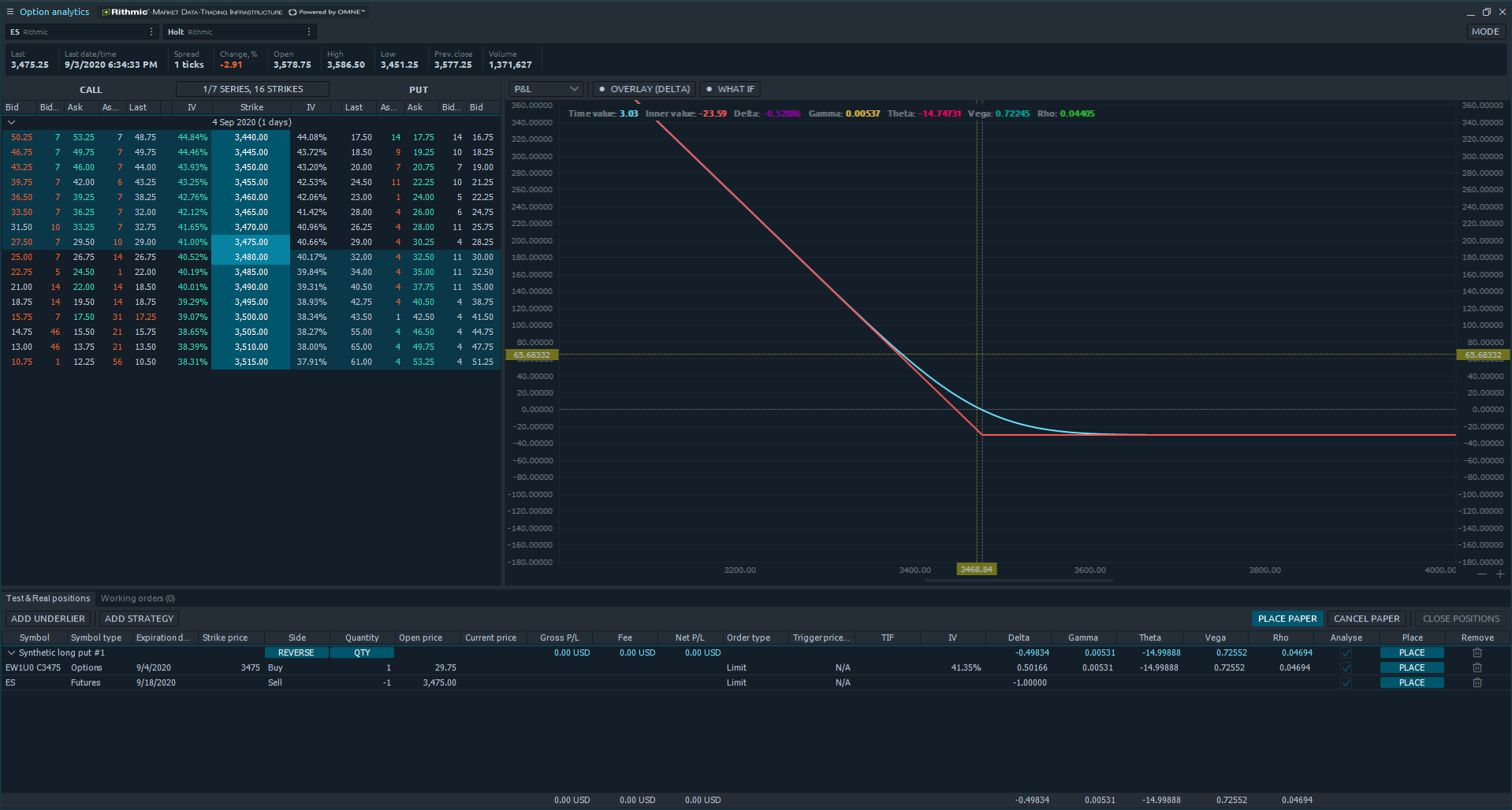

Synthetic Put

How to Construct It:

- Sell one futures contract

- Buy one ATM or slightly OTM above your selling price.

Objective: To put an “insurance policy” on your short position.

Directional Bias: Bearish

When to Use It: If you’re bearish on the market but want to cap your upside risk.

Profit Scenario: Your maximum profit is uncapped and your profit begins maximizing once your futures profit exceeds the premium you paid for the call. Calculation: Futures price – call premium.

Loss Scenario: If your futures rise in value, you take a loss, but one that’s capped by your long call. Calculation: Call strike price – futures price + call premium.

Key Concepts:

- You profit the most if your futures contract has an explosive move downward.

- Your downside is limited by your long call position.

Collar

How to Construct It:

- Buy one futures contract

- Buy one ATM or OTM put

- Sell one OTM call

Objective: To execute a lower-risk long position over a lengthier period of time.

Directional Bias: Bullish

When to Use It: When you have a longer-term bullish outlook that may take time to develop, entailing downside volatility.

Profit Scenario: Your maximum profit occurs when your futures position exceeds your short call strike price. Profitability depends on the strike prices and premiums you execute for your out and call. Calculation: Call strike – put strike – the risk of the trade

Loss Scenario: Your loss is capped, but the amount will vary according to the strike prices and premiums you execute.

Key Concepts:

- Collars are net capital gains trades that emphasize downside protection more so than maximize profit potential.

- Depending on how you execute the trade, your short call premium will offset some of the cost of the purchased put.

Bull Spread

How to Construct It:

- Buy one lower strike call

- Sell one higher strike call

Objective: To reduce the cost of a long call while capping your maximum profit potential.

Directional Bias: Bullish.

When to Use It: When you have a long bias but would like to reduce the cost of your long premium, understanding that you also limit your profit potential by selling a higher strike call.

Profit Scenario: Maximum profit occurs when the underlying exceeds the higher strike price. Calculation: Difference in strikes – net debit.

Loss Scenario: If the underlying declines, you will lose your entire premium on the lower strike call but this will be offset by the higher strike call premium that you sold. Your maximum loss os the net debit paid.

Key Concepts:

- This is a vertical spread that reduces your profit potential but also reduces your net debit (or cost of trade). Your profit and loss potential will vary depending on how far apart the strike prices are; the wider, the greater potential for profit and loss.

Bear Call Spread

How to Construct It:

- Sell one call at a strike price above the underlying price.

- Buy one OTM call at a higher strike price.

Objective: To place a bearish trade that aims to collect income while calling your risk should the underlying move higher in price.

Directional Bias: Bearish.

When to Use It: When you forecast the underlying futures are about to decline.

Profit Scenario: If the underlying declines, staying well below the lower short call, you’re likely to receive your maximum income credit. Calculation: Net credit received.

Loss Scenario: If the underlying price moves higher, your risk is capped once the underlying exceeds the higher “long” call’s strike price. Calculation: Difference in strikes – net credit.

Key Concepts:

- This bear call spread is a short-term income strategy.

- The caveat in this trade is that your maximum risk is typically higher than your maximum profit potential in income received.

Calendar Call

How to Construct It:

- Buy one call with a longer-term expiration date.

- Sell one call of the same strike price but at near-term expiration date.

Objective: To generate income while you’re holding a longer-term position by collecting the premium on the near-term call.

Directional Bias: Neutral to bullish.

When to Use It: When you’re bullish over a longer time horizon but the underlying appears to be stagnating.

Profit Scenario: If the price remains stagnant, you collect premium; if implied volatility rises, the value of your longer-term premium increases. Calculation: Long call value at the time of the short call expiration, when the Futures

price is at the strike price – net debit.

Loss Scenario: Maximum loss of net debit paid occurs if the underlying price moves sharply up or down beyond your strike price.

Key Concepts:

- Calendar call is a variation of the covered call.

- A calendar call is an effective way to potentially collect income against a longer-term bullish position.

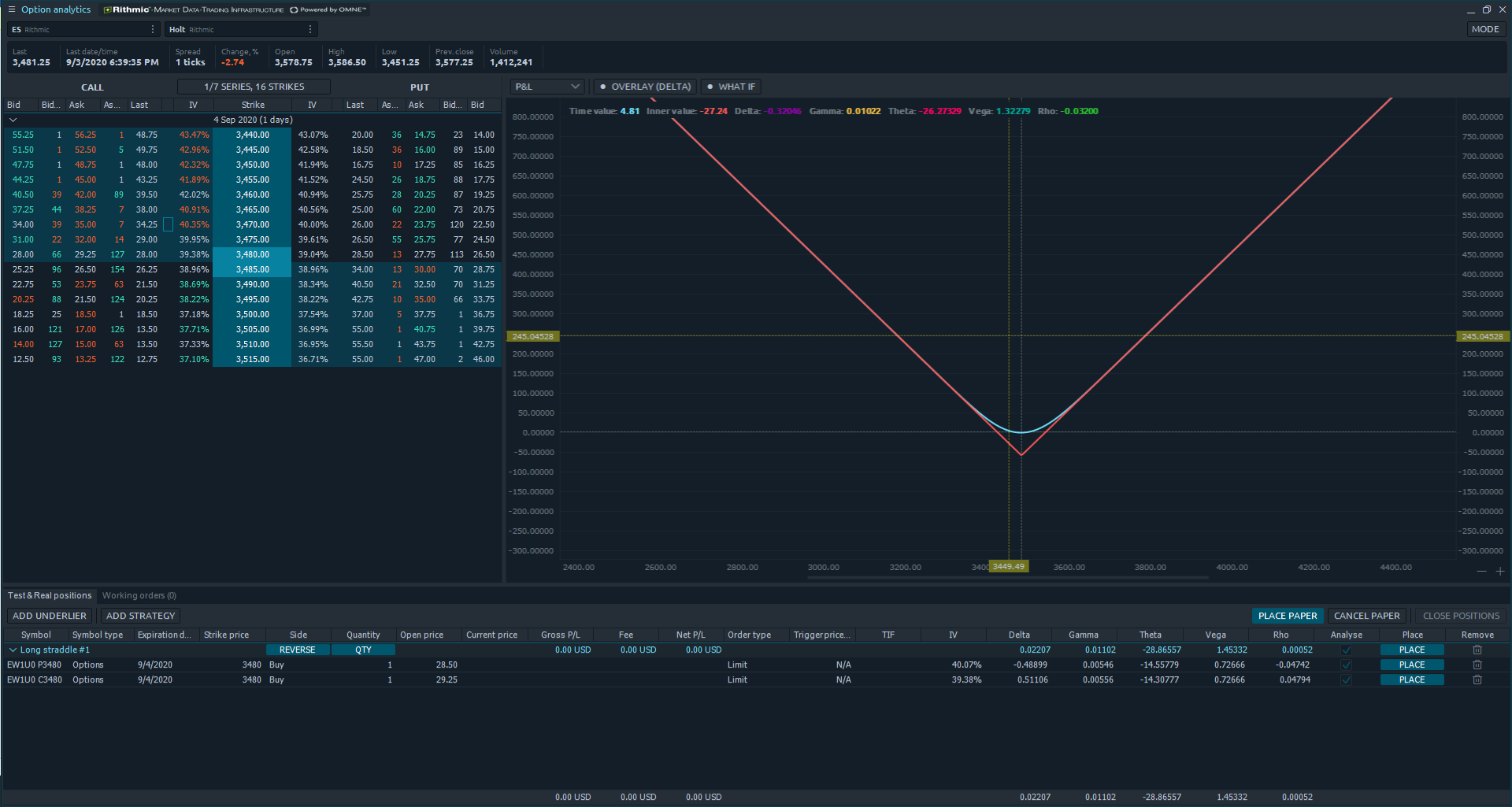

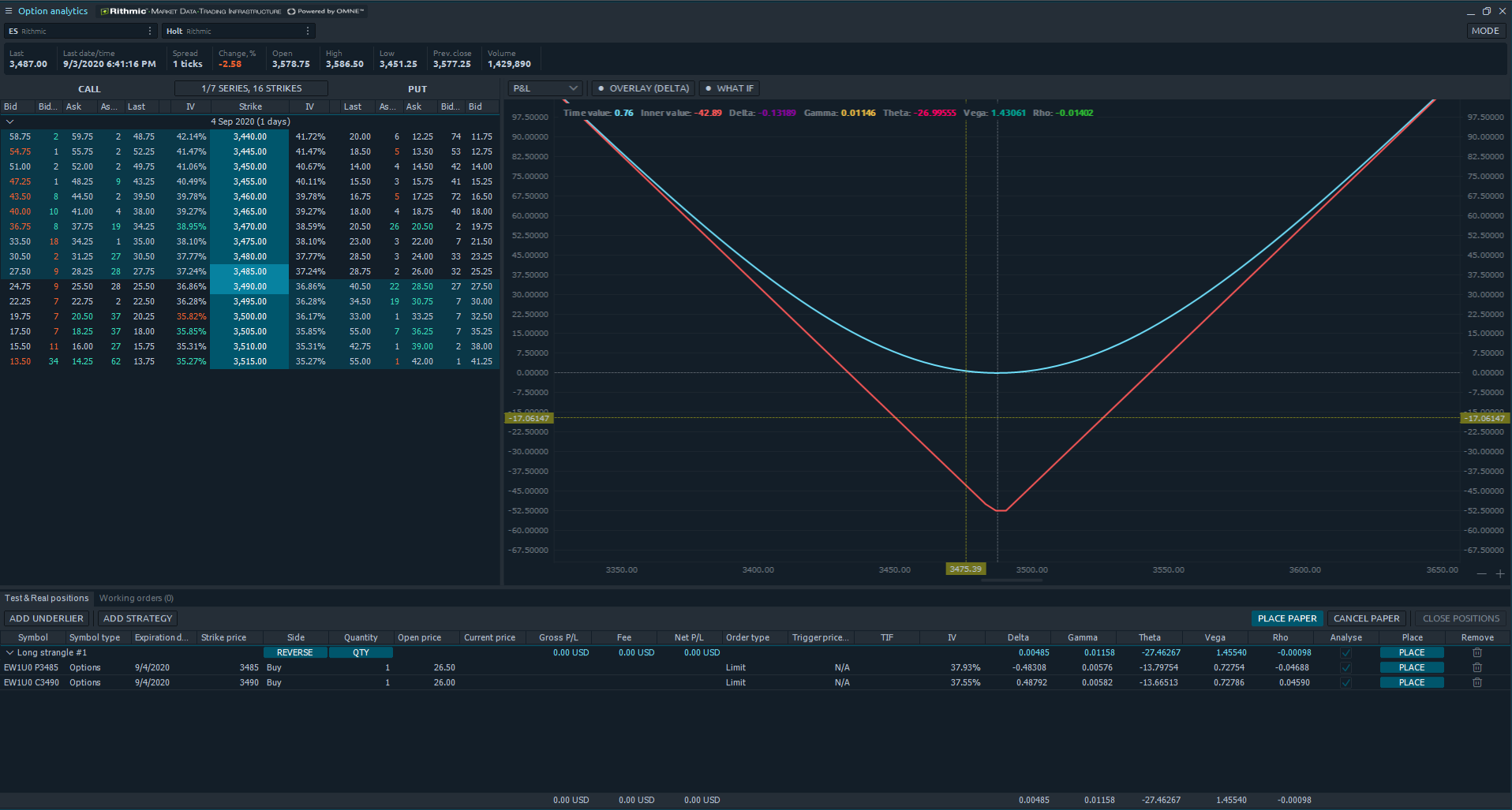

Long Straddle

How to Construct It:

- Buy one ATM call

- Buy one ATM put with the same strike price and expiration

Objective: To exploit a large move in either direction, up or down.

Directional Bias: Neutral, as you may profit in a volatile move in either direction.

When to Use It: When you believe the underlying is bound for a major breakout in either direction before contract expiration. Some traders prefer to execute this trade before a major economic release that can move the underlying.

Profit Scenario: Maximum profit occurs when the underlying moves above or below the breakeven range. The profit potential for this trade is theoretically unlimited.

Loss Scenario: If the underlying stays within the breakeven parameters by expiration, then your maximum loss is the net debit amount you paid.

Key Concepts:

- When constructing a straddle, you’re assuming that the underlying is poised for a volatile move in one direction, whether it is up or down.

- SInce this is a net debit trade, time decay plays a significant role in any profit scenario, as premiums tend to erode the longer you hold a position toward expiration.

Short Straddle

How to Construct It:

- Sell one ATM call

- Sell one ATM put with the same strike price and expiration

Objective: To collect income using a direction-neutral strategy where the implied volatility is expected to decline.

Directional Bias: Neutral; sideways.

When to Use It: When you anticipate the implied volatility of an underlying is high and set for a decline in a sideways or range-bound market.

Profit Scenario: If the underlying stays within the breakeven range, your maximum profit is the net credit received on the trade.

Loss Scenario: If the underlying exceeds the breakeven range in either direction, your maximum loss is potentially unlimited

Key Concepts:

- The short straddle is an income strategy that’s best used in a sideways market.

- The higher the implied volatility at the opening of the trade, the larger your potential credit income.

- Preferably, you might consider executing this trade close to expiration, when you anticipate that the volatility might decrease significantly.

Long Strangle

How to Construct It:

- Buy one (higher) OTM call

- Buy one (lower) OTM put with the same expiration

Objective: To execute a direction-neutral trade for capital gain when the underlying undergoes a volatility move in either direction.

Directional Bias: Neutral, assuming volatility picks up.

When to Use It: When you anticipate that the underlying is poised for a significant breakout in either direction before expiration. Some traders prefer to execute this trade before a major economic release that can move the underlying.

Profit Scenario: Maximum profit occurs when the underlying moves above or below the breakeven range. The profit potential for this trade is theoretically unlimited.

Loss Scenario: If the underlying stays within the breakeven parameters by expiration, then your maximum loss is the net debit amount you paid.

Key Concepts:

- Similar to a straddle, you’re assuming that the underlying is poised for a volatile move in one direction, whether it is up or down.

- Since this is a net debit trade, time decay plays a significant role in any profit scenario, as premiums tend to erode the longer you hold a position toward expiration.

Short Strangle

How to Construct It:

- Sell one (higher) OTM call

- Sell one (lower) OTM put with the same expiratio

Objective: Similar to a short straddle, you execute this income trade when you anticipate the implied volatility of an underlying is high and set for a decline in a sideways or range-bound market.

Directional Bias: Neutral.

When to Use It: When you anticipate the implied volatility of an underlying is high and set for a decline in a sideways or range-bound market.

Profit Scenario: If the underlying stays within the breakeven range, your maximum profit is the net credit received on the trade.

Loss Scenario: If the underlying exceeds the breakeven range in either direction, your maximum loss is potentially unlimited.

Key Concepts:

- Similar to the short straddle, the short strangle is an income strategy that’s best used in a sideways market.

- The higher the implied volatility at the opening of the trade, the larger your potential credit income.

- Preferably, you might consider executing this trade close to expiration, when you anticipate that the volatility might decrease significantly.

Long Iron Butterfly

How to Construct It:

- Buy one higher OTM call

- Sell one middle ATM call

- Sell one middle ATM put

- Buy one lower OTM put

Objective: To execute a high yielding credit trade where you anticipate the underlying to close within the medium range of your outer (OTM) strikes.

Directional Bias: Sideways.

When to Use It: When you anticipate the underlying trading in a range-bound manner.

Profit Scenario: Your max profit occurs when the underlying closes within the upper and lower bounds of your long (call and put) strike prices. Your maximum profit is the net credit received.

Loss Scenario: Maximum loss occurs if the underlying closes at either end of long options’ strike prices. Calculation: Difference in adjacent strikes – net credit.

Key Concepts:

- When you trade the long iron condor, you’re anticipating range-bound motion.

- A credit trade, you’ll receive more credit when implied volatility is high and subsequently declines.

Short Iron Butterfly

How to Construct It:

- Sell one higher OTM call

- Buy one middle strike ATM call

- Buy one middle strike ATM put

- Sell one lower OTM put

Objective: To execute an “inexpensive” yet capped yield trade where you anticipate the Futures contract to finish on either side of the upper or lower strike prices.

Directional Bias: Neutral, assuming there will be a movement toward either strike price.

When to Use It: When you feel that the underlying will move toward either strike price by expiration.

Profit Scenario: Maximum profit occurs when the underlying closes at or above/below the short strike prices.Calculation: Difference between adjacent strikes – net debit.

Loss Scenario: If the underlying price remains within the middle range, your maximum loss is the net debit paid.

Key Concepts:

- The goal behind this trade is to execute an inexpensive long-volatility position whose maximum loss is capped.

Long Iron Condor

How to Construct It:

- Buy one higher strike OTM call

- Sell one higher middle strike OTM call

- Sell one lower middle strike OTM put

- Buy one lower strike OTM put

Objective: To execute a high-yielding trade with net credit, preferably in a low volatility environment.

Directional Bias: Sideways.

When to Use It: When you anticipate the underlying trading in a range-bound manner.

Profit Scenario: Your max profit occurs when the underlying closes within the upper and lower bounds of your long (call and put) strike prices. Your maximum profit is the net credit received.

Loss Scenario: Maximum loss occurs when the underlying closes above the long call or below the long put. Calculation: Difference in adjacent strikes – net credit.

Key Concepts:

- Perhaps it’s safest to trade this strategy on a shorter-term basis with one month or less to expiration.

- The long iron condor is a way to collect a premium for a ranging underlying while capping your risk and potential losses, should the trade work against you.

Short Iron Condor

How to Construct It:

- Sell one higher strike OTM call

- Buy one middle strike OTM call

- Buy one middle strike OTM put

- Sell one lower strike OTM put

Objective: To execute an inexpensive yield trade that aims to exploit an increase in volatility.

Directional Bias: Neutral (up or down).

When to Use It: When you anticipate the underlying to increase in volatility in either direction.

Profit Scenario: Maximum profit occurs when the underlying exceeds either strike price by expiration.

Loss Scenario: Maximum loss occurs if the underlying fails to move beyond the breakeven level at either end of the short strike prices. Your maximum risk is your net debit paid.

Key Concepts:

- The short iron condor strategy is a “long volatility” play.

- Although your risk is capped, the underlying must be volatile enough to move in either direction beyond the outer strikes.

- The risk-to-reward scenario is skewed toward risk, as the amount that you can lose is greater than the amount that you can profit.

Click Here to view our selection of Options Futures Trading Platforms that, in our opinion, are most appropriate for short-sellers and spreads traders of Options Futures.

There is a substantial risk of loss in futures trading. Past performance is not indicative of future results.

IF YOU PURCHASE A COMMODITY OPTION YOU MAY SUSTAIN A TOTAL LOSS OF THE PREMIUM AND OF ALL TRANSACTION COSTS

A “SPREAD” POSITION MAY NOT BE LESS RISKY THAN A SIMPLE “LONG” OR “SHORT” POSITION

IF YOU PURCHASE OR SELL A COMMODITY FUTURES CONTRACT OR SELL A COMMODITY OPTION YOU MAY SUSTAIN A TOTAL LOSS OF THE INITIAL MARGIN FUNDS OR SECURITY DEPOSIT AND ANY ADDITIONAL FUNDS THAT YOU DEPOSIT WITH YOUR BROKER TO ESTABLISH OR MAINTAIN YOUR POSITION.

CME Micro contracts generally have a value and margin requirement that is one-tenth (10%) of the corresponding regular contract. The cost of trading Micro contracts is higher than regular contracts when measured as a percentage. Commission rates are not always one-tenth of the rate for regular contracts. Exchange and NFA fees are not proportionately reduced. Frequent trading of Micro contracts further compounds the cost disparity. Futures transactions are leveraged, and a relatively small market movement will have a proportionately larger impact on deposited funds. This may result in frequent and substantial margin calls or account deficits that the owner is required to cover by depositing additional funds. If you fail to meet any margin requirement, your position may be liquidated, and you will be responsible for any resulting loss.